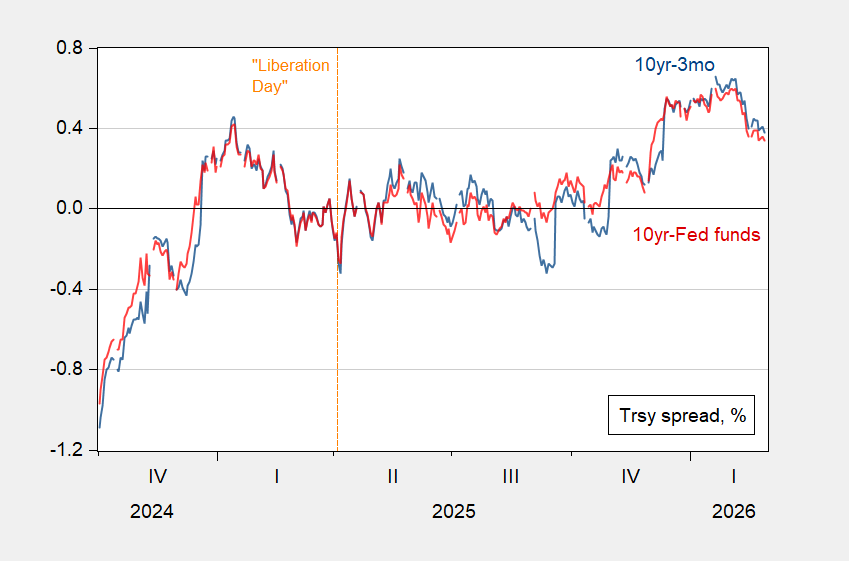

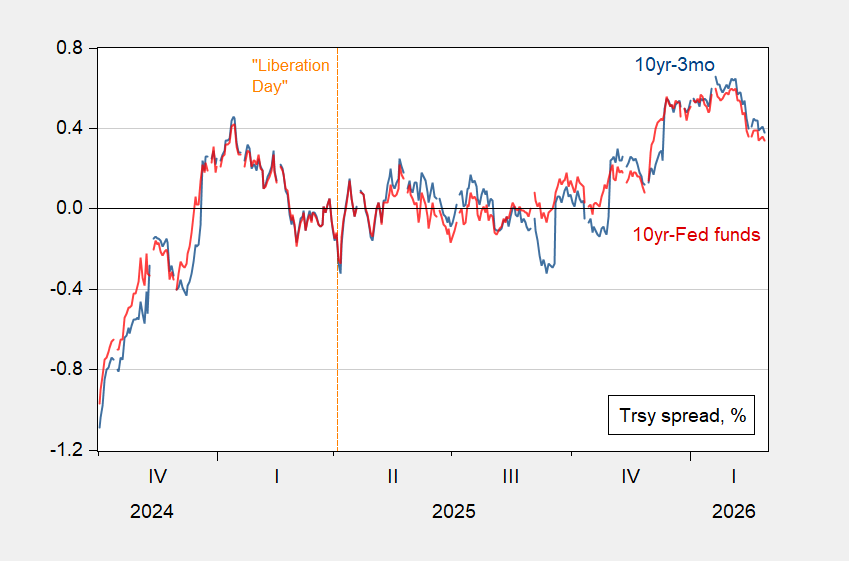

At high frequency, the 10yr-3mo and 10yr-Fed funds spreads are shrinking:

What to think of this? Typically, we decompose the (risk free) Treasury long yield as:

tp is the term premium. However, the default risk on Treasurys have been relatively high over this period.

For comparison, 5 year German CDS are at 7.7. US 5 year CDS were under 10 early in Biden’s term.

If we could adjust for inflation risk (as DKW do, but only through January 31) and default risk, the resulting adjusted term spread might be even smaller. Adjusting for the inflation risk, the 10yr-3mo would be 25 bps instead of 36, using the end-January difference.