This is Naked Capitalism fundraising week. 997 donors have already invested in our efforts to combat corruption and predatory conduct, particularly in the financial realm. Please join us and participate via our donation page, which shows how to give via check, credit card, debit card, PayPal, Clover, or Wise. Read about why we’re doing this fundraiser, what we’ve accomplished in the last year, and our current goal, bonuses for our esteemed writers.

Your humble blogger is no expert in French politics. I trust those who are will pipe up.

But from this far remove, it looks as if President Macron’s days are numbered. Even though his term in office lasts until May 2027, the record-speed collapse of the government of Macron’s latest Prime Minister pick Sébastien Lecornu had formed a government suggests that even with the office of the French President being extremely well bunkered against challenges from the Parliament, that Macron’s position has become so untenable that he can’t hold out for much longer.

First some hot takes. From LeMonde:

President Emmanuel Macron’s office announced that Prime Minister Sébastien Lecornu had tendered his resignation on the morning of Monday, October 6, hours after his new government had been formed. Lecornu’s resignation after 27 days in office, making him the shortest-lived prime minister in modern French history, plunges the country into political uncertainty again….

On Sunday evening, Lecornu had unveiled his cabinet, which was almost identical to that of his fallen predecessor, François Bayrou. But cracks were apparent right away, with members of several parties within the governing coalition expressing doubts and criticism about the lack of change….

It was not immediately clear how Macron would proceed. Up to now, he has resisted calls to again order new snap legislative polls and has also ruled out resigning himself before his mandate ends in 2027…

Jean-Luc Mélenchon, the leader of the radical-left La France Insoumise (LFI) party, called to introduce a motion to remove Macron from office. Mathilde Panot, a prominent member of LFI, called for Macron’s resignation following Lecornu’s resignation. “The countdown has begun. Macron must go,” she said, in a post on X.

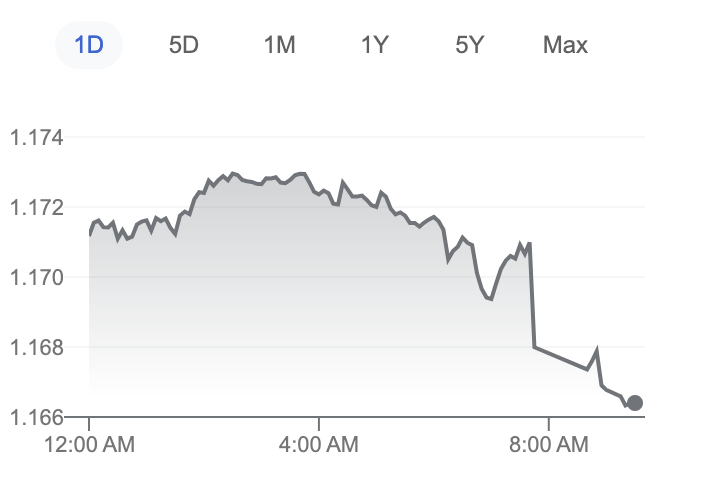

The Paris stock market had slipped by more than 2% by 10 am, half an hour after the news broke.

The euro has also weakened against the dollar, and that looks to have been triggered by the shock resignation:

From the Financial Times:

France’s Prime Minister Sébastien Lecornu has resigned less than a month after his appointment, prompting a market sell-off amid concern about dysfunction in the Eurozone’s second-biggest economy…

His resignation came after his allies in the centre-right Les Républicains indicated they could withdraw from his government because of the number of ministers he planned to include from Macron’s Renaissance party.

The leftwing Socialist party also threatened to vote it down unless Lecornu suspended Macron’s emblematic pension reforms.

Lecornu was the third prime minister appointed by Macron since snap parliamentary elections in summer 2024, a vote that left the French assembly bitterly divided and has made governing almost impossible. All three have now left office….

Macron will have the difficult challenge of either naming another prime minister who is likely to encounter the same difficulties as Lecornu and his predecessors, or calling new parliamentary elections…

“The only way to stop this crisis is to have a new election,” said Emmanuel Cau, head of European equities strategy at Barclays. “It’s making Europe hard to invest in and creating an excuse for investors to tread carefully.”

He added: “The market has to think about the far right being in a position to capitalise.”

The additional interest rate paid on French debt over benchmark German Bunds — a closely watched measure of market worries — went as high as 0.88 percentage points, close to its highest level since the Eurozone debt crisis more than a decade ago.

And the Wall Street Journal:

The failure of yet another Macron government is a sign of the dwindling options the president faces as he tries to rein in France’s ballooning budget deficit while corralling a fractious National Assembly.

France’s borrowing costs have risen to the levels of Europe’s debt-laden periphery as Macron has cast about for a prime minister who can pass a new budget by the end of the year. France’s CAC 40 stock index fell 2% on Monday while the yield on France’s 10-year bonds rose to 3.6%, above Italy’s.

Macron faced immediate demands to dissolve the National Assembly and call parliamentary elections from opponents who say the lower house is too fractured to produce a stable government.

“There can be no return to stability without a return to the polls and the dissolution of the National Assembly,” said Jordan Bardella, the president of the far-right National Rally, on Monday.

Fresh elections risk further diminishing Macron’s ranks in the National Assembly. His decision to dissolve parliament in the summer of 2024 paved the way for the current fragmentation, with parties on the left and far right gaining seats while Macron’s centrist and conservative allies suffered losses….

Lecornu took office promising a break with Macron’s previous prime ministers. But he was quickly engulfed in the storm that doomed his predecessors, with lawmakers on the left demanding tax increases on the wealthy to close the budget gap and lawmakers on the right blaming France’s sizable welfare state for the fiscal mess. Neither side showed signs of budging, let alone supporting Lecornu’s efforts to form a cabinet from different parties that might help build consensus across the National Assembly.

Instead, Lecornu appointed figures drawn from previous Macron governments. He named former Finance Minister Bruno Le Maire as defense minister, enraging conservatives who blamed him for the state of France’s public finances.

Lawmakers on the left, meanwhile, took aim at Lecornu for sticking with Macron loyalists, undermining his promise for a break with the past.

Throughout the crisis, Macron has refused to appoint a prime minister from a coalition of leftist parties that won the most votes in 2024’s snap election. Since then, the coalition—which ranges from the far-left France Unbowed to socialists and greens—has become consumed with infighting. That makes it hard for Macron to name someone on the left who could muster a majority in parliament.

The question implied in the Journal extract, and often discussed more bluntly elsewhere, is whether France has become “ungovernable”. As far as the current impasse is concerned, the very high level summary is that France has been running large fiscal deficits for many year to support its social safety nets, which French citizens object viscerally to having trimmed much. France does not issue its own currency, so its ability to carry on this way (independent of getting away with violating EU budget rules) has consequences more quickly than for a currency issuer like the US or UK, in the form of having to pay a lot more in interest to be able to borrow. But France is unwilling or unable to tax meaningfully more (it is over my pay grade as to whether there are other ways to tax the well-off more besides the wealth tax idea that Macron is rejecting). And another layer of problems results from the neoliberal allergy to industrial policy to help spur growth (France does have a history of dirigisme, so it may be a bit less reluctant, but Macron himself is a neoliberal diehard, plus even with a sound plan, it would take years for a restructuring to bear real fruit).

Again, from my considerable remove, is that one solution for the budget impasse would be to do the utterly unthinkable and reject the self-serving US calls for much bigger NATO commitments, to be used significantly to bleed Europe through higher purchases of US weapons (even charitably assuming we can make all that many). But weak leaders, from Macron to Starmer and Merz, have been trying to whip up hysteria about Russia to a fever pitch so as to shore up their faltering positions. Their fear-mongering has been duly amplified by Ursula von der Leyen and one imagines many members of the European parliament. So there are real fissures, even though it’s easy to caricature them as elites v. ordinary citizens. Keep in mind that the Creel Commission first demonstrated that sustained propaganda campaigns do produce large shifts in public sentiment in remarkably short periods of time.

Additional tidbits from Twitter:

Lecornu arrive même à battre un record centenaire de la Troisième république, faut applaudir pic.twitter.com/LEG9myBby2

— Julien (@Teidix) October 6, 2025

🚨🇫🇷 FLASH

Sébastien Lecornu détient un DOUBLE RECORD : le Premier ministre le PLUS LENT à FORMER son GOUVERNEMENT (26 jours), et le PLUS RAPIDE à DÉMISSIONNER (27 jours). https://t.co/RqdOfk3Nvm pic.twitter.com/nz2MnYTFIy

— Impact (@ImpactMediaFR) October 6, 2025

Note that this continued revolt against Macron’s neoliberal, pro-war budget policies comes on the heels of a different process of government formation, with former Czech prime minister Andrej Babis set to return to power.

From Bloomberg:

- Billionaire Andrej Babis is set to form a new Czech government after scoring his best-ever election victory, with plans to govern with the support of a far-right group and a populist party.

- Babis’s return to power is poised to bolster the ranks of populist leaders in the European Union, with his campaign putting Brussels on notice that he will challenge policies from migration to military aid to Ukraine.

- Babis has made clear that he is against any form of “Czexit” and remains an adherent of NATO, but his policy agenda is expected to lie with his allies, including Hungarian Prime Minister Viktor Orban and Slovakia’s Robert Fico.

Note a Bloomberg piece sees the whackage to the euro to be limited:

Still, once the knee-jerk reaction fades, France’s political risks may have limited power to drag the currency lower. Markets have shown little sensitivity to such headlines in recent weeks, and today’s move likely reflects traders jumping on the first tradeable story in days, with the US shutdown keeping dollar visibility low. Options pricing, meanwhile, continues to show a constructive bias on the euro’s short-term outlook.

To keep the discussion focuses on “whither France?” we do need to dismiss one issue, that of a Eurozone breakup. The UK demonstrated that countries that kept their own currencies can exit the EU, albeit with real and not trivial economic costs. Eurozone members like France are in a completely different place. We can unpack this again (we treated it repeatedly and at length during the Greek bailout crisis of 2015), but the short version is trying to leave the Eurozone would produce an immediate banking system collapse. There is no way to do it quickly. As soon as word goes out, those with deposits in French banks would immediately move them to other banks in the eurozone, or even completely outside the EU, to escape having their deposits force-redenominated into a new franc that would be sure to be worth less outside France than euros. In addition, the French government’s ability to force-redenominate borrowings in euros on its own behalf and on behalf of private parties into new francs would also likely be limited. Any exposed borrowers would see the real value of their debts rise, since they would have to continue paying in euros even though their assets, and presumably a lot of their income, would be in lower-value new francs.

Mind you, the above does not mean that non-Eurozone members might not at some point gear up to leave the EU. But NATO, which legally is a loose alliance and heavily dependent on the US, IMHO is more at risk.